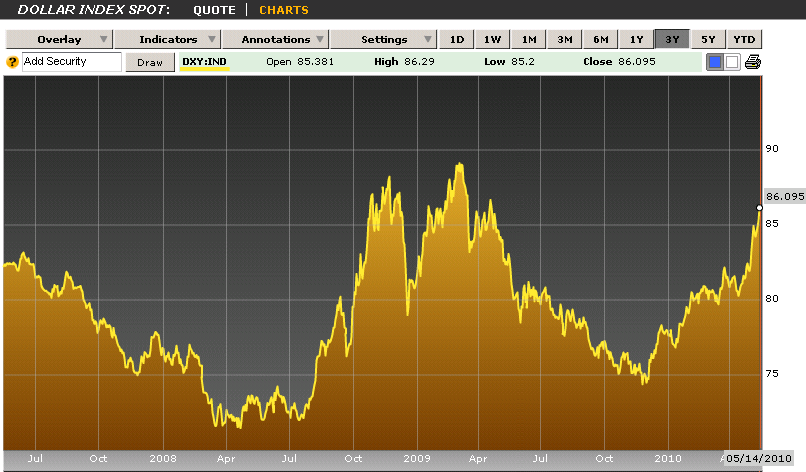

The fiscal crisis ravaging the Euro and the Pound has sent the Dollar skyward. On the one hand, the prospect of continued uncertainty and dissolution of the Euro would seem to be an excellent harbinger for continued appreciation in the Dollar. On the other hand, it should only be a matter of time before investors recognize that the Dollar’s fiscal fundamentals are also quite weak.

Unlike during the last few years, analysts are no longer talking about (forex reserve) diversification. It was once widely predicted that the Euro would rival the Dollar for a place in the portfolios of foreign Central Banks. As expected, preferences are now shifting back in favor of the Dollar and to a lesser extent, the Yen. The Pound and Swiss Franc may have a small role, as will the “New†Euro. Over the short-term, however, Central Banks (and investors) will continue to eschew the Euro, if only due to sheer uncertainty.

Given that everything is relative in forex, investors and Central Banks only have so many options when it comes to choosing which currencies in which to denominate their portfolios. Thus, it’s understandable that a sudden crisis in the EU would buoy the Dollar. At the same time, it’s not exactly a good bet that the US isn’t destined to suffer a similar fate.

Due to extremely low short-term interest rates, most investors have been willing to accept low returns when lending to the US (by buying Treasury Securities, and indirectly by simply holding Dollars). At some point, both short-term interest rates and the rate of inflation will rise, and investors will have to re-examine their risk/reward schemes. My suspicion is that investors will demand higher yields in exchange for lending to the US.

Just like with Greece, a US fiscal crisis would probably emerge suddenly. While the US government pays lip service to the notion of balancing its budget and reducing its sovereign debt, even the most optimistic projections show a budget deficit for the next 10 years. Beyond that, the retirement of the baby boom generation and their “entitlement†payment will make it nearly impossible for the US to operate a budget surplus.

In short, the only hope is for the US economy to grow faster than the national debt. If the US economy grows at 4% per year, for example, it will have to run a budget deficit less than 4% of GDP in order to reduce its relative level of debt. On the surface, this seems like a reasonable possibility, but given trends over the last three decades (covering periods of both recession and economic boom), it doesn’t seem likely.

This is not new information. Doomsday theorists have been predicting the bankruptcy of the US for two centuries. Don’t mistake me for doing the same. Rather, I only wish to point out how ironic it is that the Dollar’s fiscal conditions are comparable (and in some ways worse) than some of the problem countries that investors are currently focusing on.

Then again, forex is relative. Some analysts have suggested that the new reserve currency will be gold, oil, and other commodities. Unfortunately, there isn’t nearly enough (liquid) supply of these materials to occupy more than a small portion of reserves. Under the current system, then, investors are pretty much stuck with the Dollar. At this point, betting to the contrary is tantamount to betting on the complete collapse of the modern financial system. A reasonable bet, perhaps, but you can forgive investors for being hesitant to embrace it.

Powered by WizardRSS | Full Text RSS Feeds

No comments:

Post a Comment